This page may contain compensated affiliate links. Please read my disclosures for more details.

Here are answers to the most commonly asked questions about The Money Tracker! If you have questions that aren’t answered here, please reach out to me on via my contact form and let me know what else you’d like me to cover here!

1. How do I track credit accounts with no minimum payment / changing monthly payments?

2. Where should I enter my credit card payments on The Money Tracker?

9. How do you account for due dates of upcoming bills?

Return to Money Tracker download page

How do I track credit accounts with no minimum payment/changing monthly payments?

A READER ASKS

One question I do have is the most logical way to handle accounts with no minimum payment/changing autodraft. We use/abuse Amazon A LOT and have an Amazon card with an automated draft for most purchases there. I can and do go through and track the individual purchases and categorize them, but then the previous month’s purchases get taken out in a large payment that affects our account balance in a big way. Just wondering if there is an easier/more logical way to track everything to figure out how we’re spending and get the big autopay in there too without having everything show up twice!

Is there an easier/more logical way to track everything to figure out how we’re spending and get the big autopay in there too without having everything show up twice! What is the most logical way to handle accounts with no minimum payment/changing auto drafts?

AVERY SAYS

I know what you mean about the big hit to your account balance when the previous month’s payments get paid off. It sounds like you’ve thoroughly thought this through, but just in case the below info is useful, I’ll put it out there…

With the credit cards I use, I’ve found that once the budget gets to the stage where you’re confident on what you can comfortably afford for expenses and get a surplus saved up as a cushion (the extra cash that shows up in the yellow Surplus-to-Date section of the Money Tracker), it no longer causes stress when you get that big credit card payment to pay off all at once. This is because the previous month’s income has already been set aside for those expenses via the Money Tracker. So you might have a large bank account balance, but you already know (via the Money Tracker) how much surplus income you actually have available to spend, and when the account balance takes a big dip after paying off the card it’s no big deal since you planned for that already.

However, in the beginning, when you’re still feeling your way through your finances, that large monthly payment definitely can be a shocker when you see your checking account balance take a plunge each time you pay it.

One alternative is to pay off that Amazon card more often – say once a week, or once every 2 weeks. That way in the beginning when you’re still figuring out how much you can afford to spend on it, the increased frequency of making payments/checking the balance will prod you to put a halt to spending on the card for that month sooner, if required.

Return to Money Tracker download page

Where should I enter my credit card payments on The Money Tracker?

A READER ASKS

Where should I enter my credit card payments on the Money Tracker?

AVERY SAYS

The answer depends on whether or not you pay off your credit cards in full each month.

What to Do if You Pay Off Your Credit Cards in Full Each Month

What I do is keep track of each individual purchase instead. So say in June I’ve charged the following to my credit card (I know this is way to short a list for real life, but I think it’ll give you the idea):

$100 at Safeway for Groceries on June 1

$50 to stock up on toilet paper and kleenex at Walmart on June 5

$60 to buy gas for my car on June 8

Pretend those are the only things I’ve charged to the credit card that month.

I’d enter $100 under the groceries column of the blue expenses section.

I’d enter $50 under the household supplies column of the blue expenses section.

I’d enter $60 under the transportation column of the blue expenses section.

Then when I actually pay off the $210 in charges on my credit card, there’s no need to enter that in the Money Tracker since I’ve already accounted for that spending earlier.

Say you mess up one month and accidentally pay a bit late and have to pay interest charges – the amount you paid in interest will show up on your next statement, and you can enter the amount of interest you paid into the Money Tracker under loan payments in the blue expenses section. (Remember, the rest of the credit card payment will not need to be entered into the Money Tracker since you’ve already accounted for each individual charge via the receipts you saved from your purchases.)

So say your credit card statement showed a balance of X (doesn’t matter what the number is, since if you account for your purchases with the individual receipts, you’ve already tracked whatever made up that balance), and interest charges of $40.

The only thing you’d have to enter into the Money Tracker from your credit card statement is the $40 in interest, which I’d put in the Loan Payments section of the blue expenses section.

What to Do if You Have NOT Been Able to Pay Off Your Credit Cards in Full Each Month

Ok, so this situation can be complicated, depending on how you approach it. There’s an easy way to deal with it, and a hard way – but both work. So stick with me as I explain both options, then choose the one that you prefer. 😃 Here goes…

Now say things are more complicated and prior to reading the book, you’ve amassed a significant amount of credit card debt that wasn’t accounted for with individual receipts in the Money Tracker as I indicated above. If that’s the case, then at the start of Month 1, contact your credit card companies to find out the balance on each card. Enter that in the orange debt section, just so you can see at a glance what you owe.

You’ve got 2 choices for tracking this going forward.

1. This is the easiest, least time-consuming route—I’d lean towards doing it this way to keep things simple. Do not charge anything else to that credit card until you’ve paid it off in full. (Instead, use your debit card or cash, save all receipts, and enter them into The Money Tracker). Then all you have to do with that credit card is enter whatever credit card payments you make as loan payments in the Money Tracker, and update the orange debt section once a month to track your progress in paying it down.

2. Keep using the credit card—some people do this to save on debit fees or continue to collect credit card reward points—but now you have to keep track of what purchases are new so you know what portion of your monthly payment went towards paying down the old debt, the interest, and new charges.

So I’m going to make up some numbers here as an example.

Say you currently carry a balance of about $5000 on your Capital One Mastercard.

Say this month you charged:

$100 at Safeway for Groceries on June 1

$50 to stock up on toilet paper and kleenex at Walmart on June 5

$60 to buy gas for my car on June 8

Pretend those are the only things you’ve charged to your Capital One Mastercard that month.

I’d enter $100 under the groceries column of the blue expenses section.

I’d enter $50 under the household supplies column of the blue expenses section.

I’d enter $60 under the transportation column of the blue expenses section.

I’d also keep a separate tally somewhere else of what amount was charged to the Capital One Mastercard, in this example, it would add up to $210.

Now when you get your Capital One Mastercard statement, say the statement shows a balance of $5290, with $70 of that being interest charges.

Option A – you can only afford to pay off the $70 interest and new charges of $210

Say you make a payment of $280 (i.e. enough to cover the $70 interest plus this month’s new charges of $210)

In this case, I’d enter $70 as loan payments in the blue expenses section of the Money Tracker, and that’s it.

You’re already tracking the $5000 balance in the orange debt section.

You’ve already tracked the $210 in new charges when you entered the gas, groceries, and toilet paper/kleenex purchases in the blue expenses section.

Option B – you can afford to pay off some of your old debt on the card, the interest, and this month’s new charges.

Say you decide to make a payment of $500.

As with Option A, you’ve already tracked the $210 in new charges when you entered the gas, groceries, and toilet paper/kleenex purchases in the blue expenses section. Also as with Option A, you’ll enter the $70 in interest charges under loan payments in your blue expenses section of the

Money Tracker.

So now you have another $220 left to track (i.e. $500 payment – $210 already accounted for – $70 in interest already accounted for = $220 left to track).

I’d take that extra $220 and enter it in the blue expenses section of the Money Tracker under loan payments. (So you’ll have 2 entries there, 1 for the interest, and one for the bonus debt that you’ve paid off).

Return to Money Tracker download page

For my credit cards, I can and do go through and track the individual purchases and categorize them, but then when I pay off the previous month’s purchases it gets taken out in a large payment that affects our account balance in a big way. Is there an easier way of doing this?

A READER ASKS

For my credit cards, I can and do go through and track the individual purchases and categorize them, but then when I pay off the previous month’s purchases it gets taken out in a large payment that affects our account balance in a big way. Is there an easier way of doing this?

AVERY SAYS

It can be a shock when you see the big hit to your account balance that results from paying off the previous month’s credit card statements.

With the credit cards I use, I’ve found that once the budget gets to the stage where you’re confident on what you can comfortably afford for expenses and get a surplus saved up as a cushion (the extra cash that shows up in the yellow Surplus-to-Date section of the Money Tracker), it no longer causes stress when you get that big credit card payment to pay off all at once. This is because the previous month’s income has already been set aside for those expenses via the Money Tracker. So you might have a large bank account balance, but you already know (via the Money Tracker) how much surplus income you actually have available to spend, and when the account balance takes a big dip after paying off the card it’s no big deal since you planned for that already.

However, in the beginning, when you’re still feeling your way through your finances, that large monthly payment definitely can be a shocker when you see your checking account balance take a plunge each time you pay it.

One alternative is to pay off that Amazon card more often—say once a week, or once every 2 weeks. That way in the beginning when you’re still figuring out how much you can afford to spend on it, the increased frequency of making payments will allow you to put a halt to spending on the card for that month sooner, if required.

Return to Money Tracker download page

When we spend money in the “special savings” accounts (the blue section of the tracker), I am guessing we don’t have to also put what we are spending the money for under the “expenses” section, otherwise we would be deducting the amount twice, is that right? I figured this because I saw that when I put down the amounts I would be saving for the month under the “special savings” accounts, it automatically deducted these amounts from my “month’s surplus” total.

A READER ASKS

When we spend money in the “special savings” accounts (the blue section of the tracker), I am guessing we don’t have to also put what we are spending the money for under the “expenses” section, otherwise we would be deducting the amount twice, is that right? I figured this because I saw that when I put down the amounts I would be saving for the month under the “special savings” accounts, it automatically deducted these amounts from my “month’s surplus” total.

AVERY SAYS

Yes, you are correct! 😃

Return to Money Tracker download page

Is there any way to add more cells to the Money Tracker, specifically under “Special Savings”, as well as “Expenses” (more specifically,” Spending”)?

A READER ASKS

Is there any way to add more cells to the Money Tracker, specifically under “Special Savings”, as well as “Expenses” (more specifically,” Spending”)?

AVERY SAYS

Unfortunately, there’s no easy way to do that in the Excel / Open Office version of The Money Tracker. Whenever more cells are added, often formulas need to be re-done since they don’t all re-calibrate properly after that kind of change is made. And then that process must be repeated on every single sheet (i.e. from the testing one all the way to the end of Month 12).

However, if you’re comfortable with troubleshooting formulas and repairing them if needed, you can customize the Google Docs version of The Money Tracker. That version gives you full freedom to modify it however you like. Just keep in mind the potential for formulas to break when you add new cells/rows/columns.

Return to Money Tracker download page

Is there any way to re-name the tabs from Month 1, Month 2 etc. to specific months of the year (ex. Jan, Feb, Mar, Apr etc.)?

A READER ASKS

Is there any way to re-name the tabs from Month 1, Month 2 etc. to specific months of the year (ex. Jan, Feb, Mar, Apr etc.)?

AVERY SAYS

Unfortunately, in the Excel / Open Office version of The Money Tracker that you have, it is not possible to re-name the sheets. The Money Tracker is password protected in order to prevent users from accidentally deleting a formula or changing the order of the sheets, which would break The Money Tracker. Because of this risk, even the version that I use from day-to-day is password protected.

However, if you’re comfortable with troubleshooting formulas and repairing them if needed, you can customize the tab names in the Google Docs version of The Money Tracker. That version gives you full freedom to modify it however you like. Just please keep in mind the potential for formulas to break when you add rename or re-order tabs. 😃

Return to Money Tracker download page

I’d like to use the Money Tracker on my Kindle Fire. Is there a version of the Open Office, Excel, or something similar I can download to my Kindle Fire or other tablet?

A READER ASKS

I’d like to use the Money Tracker on my Kindle Fire. Is there a version of Open Office, Excel, or something similar I can download to my Kindle Fire? I don’t use a computer, only my android phone & my tablet. Although Open Office downloaded to my phone, the text was too small to see!

AVERY SAYS

I did some research to try and find you a lead on an app that could offer a good solution for you. Here is what I found:

Microsoft Office: It’s got over 9000 reviews with an average rating of 4.4 / 5 starts, which is pretty awesome! Also, at the time I wrote this, it’s free to use! Hopefully it’ll stay that way! I haven’t actually used this software myself because I don’t use a tablet. But since it’s free, I figure there’s nothing to lose by trying it!

Return to Money Tracker download page

Why do you advise putting a checking/savings account balance in the first month income section as a starting balance?

A READER ASKS

Why do you advise putting a checking/savings account balance in the first month income section as a starting balance?

AVERY SAYS

That’s a good question.

You enter that just in just in case it is actually savings of some sort. I find it easier to explain things using sample numbers, so here goes.

Say you have $2000 in your checking account at the start of Month 1. As you say, you’d enter that as income for Month 1—that way, it will show up as a surplus in the “This Month’s Surplus” section of the Money Tracker. In future months, you won’t need to do this since any paychecks or other income you receive that pads your bank account will be entered into the green “Income” section individually.

But you’re right, for this first month, doing this could set things askew if you’re not careful. This money might be needed for something not yet accounted for.

Now say in Month 1 you end up getting a credit card bill of $1200 to pay off. If you go through the statement and see that all of the charges were incurred prior to the start of Month 1, then when you pay off this credit card bill, you’ll enter $1200 in the Expenses section under miscellaneous. This way, your Monthly Surplus will no longer show that $1200 as surplus.

In future months, you won’t have to enter your credit card payments as a lump expense, since you’ll have already accounted for the charges individually. Unless there is an interest charge on your credit card statement, in which case you’d have to enter that amount as an expense in the grey “Expenses” section.

On the other hand, say you pay for everything in cash… every single time—you hate credit cards and avoid them at all costs. In that case, at the start of Month 1, you need some way of accounting for the money that you started off with in your checking or savings account. So entering it as income is the simplest way of accounting for it, so that it shows as surplus cash that you have available.

Another factor to consider is whether or not the so-called “This Month’s Surplus” is actually needed for something that belongs in the blue “Special Savings” section. So say you had $2000 sitting around in your bank account at the start of Month 1, but you know you need to put aside $700 for your annual auto insurance premium that is due in 3 weeks. In that case, I’d go ahead and enter the full bank account balance of $2000 as income for Month 1 only. Then in the blue “Special Savings” section of the Money Tracker I’d label a section for “Auto Insurance” and under “Amount”, I’d enter the $700 that I know I’m about to spend on that. This will deduct that from your “This Month’s Surplus”. Then in future months, if you know you need $700 a year for that, you’ll enter $59 every month under “Amount” ($700 per year divided by 12 months) so you can save up for that in an systematic fashion.

Return to Money Tracker download page

How do you account for due dates of upcoming bills?

A READER ASKS

How do you account for due dates of upcoming bills?

AVERY SAYS

3 main ideas come to mind:

1. You can enter those bills in the money tracker in advance under expenses, so you know they’re coming up and you shouldn’t spend the money set aside for that in your bank account.

2. You can pay them early and get it over with so your bank account balance better reflects what you can actually spend.

3. You just make a mental note that those bills are coming up and keep track of it in your head until you’re ready to pay them and enter them in the Money Tracker.

Return to Money Tracker download page

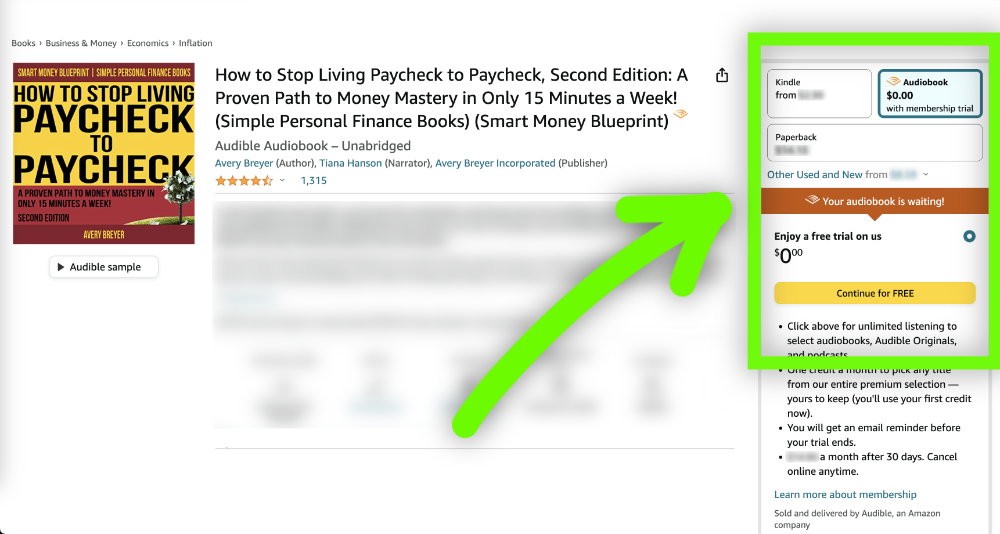

Get the audiobook—hands free listening when you’re on the go!

If you haven’t had a free trial on Amazon’s Audible lately, you may be eligible for a free trial which you can use to score a free copy of the audiobook! Check it out!

If Amazon running this promo AND you’re eligible, your screen will look something like this:

More books by Avery